The Select Committee on the Climate Crisis recently published (June 2020) a massive (547 page) & comprehensive report called “Solving the Climate Crisis”. The report was prepared by the Majority Committee Staff of the 116th US Congress pursuant to H.RES.6.

RMP is a non-partisan organization and wanted to give a review of this report as it relates to sustainable energy & put partisan politics aside. Specifically, RMP wanted to sift through some of the important parts of the report that relate to sustainable hydrogen production & storage. There is a lot of good news on the hydrogen front in this report that RMP wants to highlight as well as some themes I picked up when reading the report. First, let’s start with an overview of the whole document and then go back to themes & hydrogen specific news because there’s a lot in this mammoth report.

First the Link. The 547 page document reviewed in this post is called SOLVING THE CLIMATE CRISIS – The Congressional Action Plan for a Clean Energy Economy and a Healthy, Resilient, and Just America.

Overview:

The Executive Summary starts with the urgency of the climate crisis and how America’s ingenuity & leadership are central to solving it. In January 2019, House Resolution 6 created the bipartisan Select Committee on the Climate Crisis to “develop recommendations on policies, strategies, and innovations to achieve substantial and permanent reductions in pollution and other activities that contribute to the climate crisis.” The resolution directed the Select Committee to deliver policy recommendations to the standing legislative committees of jurisdiction for their consideration and action. Over the last 17 months, the Select Committee has consulted with hundreds of stakeholders and scientists, solicited written input, and held hearings to develop a robust set of legislative policy recommendations for ambitious climate action.

The report’s goal is to lay out congressional actions to satisfy the scientific imperative to reduce carbon pollution as quickly and aggressively as possible, make communities more resilient to the impacts of climate change, and build a durable and equitable clean energy economy. In practical terms, this means building and rebuilding America’s infrastructure, the foundation of the American economy and communities; reinvigorating American manufacturing to create a new generation of secure, good-paying, high-quality jobs; prioritizing investment where it is needed the most, including rural and de-industrialized areas, low-income communities, and communities of color; and beginning to repair the legacy of economic and racial inequality that has left low-income workers and communities of color disproportionately exposed to pollution and more vulnerable to the costs and impacts of climate change.

The document is broad & comprehensive and it is not specific to hydrogen only. Because RMP focuses primarily on hydrogen infrastructure, this post will examine the hydrogen production & storage portions of the document. Hydrogen was mentioned heavily from pages 1 to 276 along with other technologies.

Infrastructure Initiatives Related to Hydrogen Production & Storage

I recently stumbled on the terms gray hydrogen, blue hydrogen, & green hydrogen. I’m embarrassed to say I had to look up the difference between gray & blue hydrogen. As much as I follow this vector of the energy industry, I only confidently knew what green hydrogen is. Let’s go over the three basic types of produced hydrogen because they’re well differentiated through this big document and it’s very important to distinguish between them.

Gray Hydrogen = hydrogen made from natural gas

Blue Hydrogen = hydrogen made from natural gas with CO2 capture & sequestration

Green Hydrogen = hydrogen made with renewable or surplus renewable energy like solar & wind. Also, hydrogen made from renewable natural gas.

It’s important to distinguish between gray, blue, and green hydrogen for a couple reasons when reading this document as there are certain themes that develop in the first 247 pages. One of those themes is that our US Department of Energy has become “siloed” and is no longer fit to capitalize on synergies given its outdated structure with new technologies on the rise. For example, here’s a quote from page 215 & 216 discussing this key bit of information:

The applied energy offices are largely organized by fuel and focus mostly on distinct technologies rather than energy systems. This has caused potentially cross-cutting technologies to be siloed into single applications—such as carbon capture for power generation and hydrogen for transportation, despite both having potential to reduce industrial emissions—and has led to fragmented approaches for or complete disregard of other key platform technologies. Separating basic energy sciences from applied energy also prevents coordination that can help technologies move from the research stage to development and demonstration. There are multiple possible ways to restructure DOE, and many experts disagree on the best method. Some proposals include keeping basic and applied energy research under one Under Secretary to maintain their coordination and organizing applied energy offices by end-use sector rather than fuel. The reorganization should seek to create a structure that is best suited for accomplishing the updated DOE mission of decarbonization and climate mitigation, as recommended above.

That’s one of the key take aways from the document with regard to reorganizing our energy department to coordinate efforts with CO2 capture & hydrogen production as outlined on page 215-216 above. This is an important thing to note before we look at several key passages of the document as they relate to “blue hydrogen“. Blue hydrogen plays a key role in the first 247 pages especially as it relates to industrialized sectors of the economy and the people that live near industrialized urban areas. Ports are a great example of places that produce tons of noxious fumes that could benefit from blue hydrogen now as green hydrogen sources are developed. Another example of where blue hydrogen can play a key role is in steel making. We have the hydrogen technology now to strip CO2 from CH4 & sequester it in geologic formations (as RMP wrote about #CCS in Michigan here). This “blue hydrogen” can be used to make steel with 90% less CO2 emissions and almost negligible SOx, NOx, & Hg.

Another key thread through the first 247 pages is how hydrogen is not taking a back-seat to any other technology. The myth of hydrogen versus battery is starting to fade and be replaced by the more common sense approach of hydrogen & batteries working together. Hydrogen is mentioned in tandem with other technologies throughout the report with dignitas. In fact, in the urban industrial energy section of the document, hydrogen seems to be the only technology that gets talked about for decarbonized energy (e.g steel making & ammonia). Hydrogen & batteries are cousins and work together, not against one another.

Let’s look at some key “clips” from this big document to highlight the major points. The number one point, the only point that can truly move the needle for clean energy, is money money money. The “ITC” or investment tax credit has always been the #1 most important thing where the rubber hits the road. Let’s look at this first & most important clip talking about the ITC for hydrogen production & storage technology.

Clip from page 57:

Currently, storage is not independently eligible for an ITC. Rep. Michael Doyle (D-PA) and Sen. Martin Heinrich (D-NM) introduced the Energy Storage Tax Incentive and Deployment Act of 2019 (H.R. 2096/S. 1142), which would create an energy storage ITC for batteries, compressed air, pumped hydropower, hydrogen, thermal energy storage, regenerative fuel cells, flywheels, capacitors, and superconducting magnets. Section 102 of the GREEN Act of 2020 (H.R. 7330) would expand the ITC to include energy storage technology and extend the ITC so that energy storage technologies are eligible for a 30% ITC through 2025. The bill would phase down the ITC to 26% in 2026 and to 22% in 2027. Section 104 of the bill would allow taxpayers to choose a lower tax credit value in exchange for the option to be refunded for any resulting overpayment (“direct pay”).

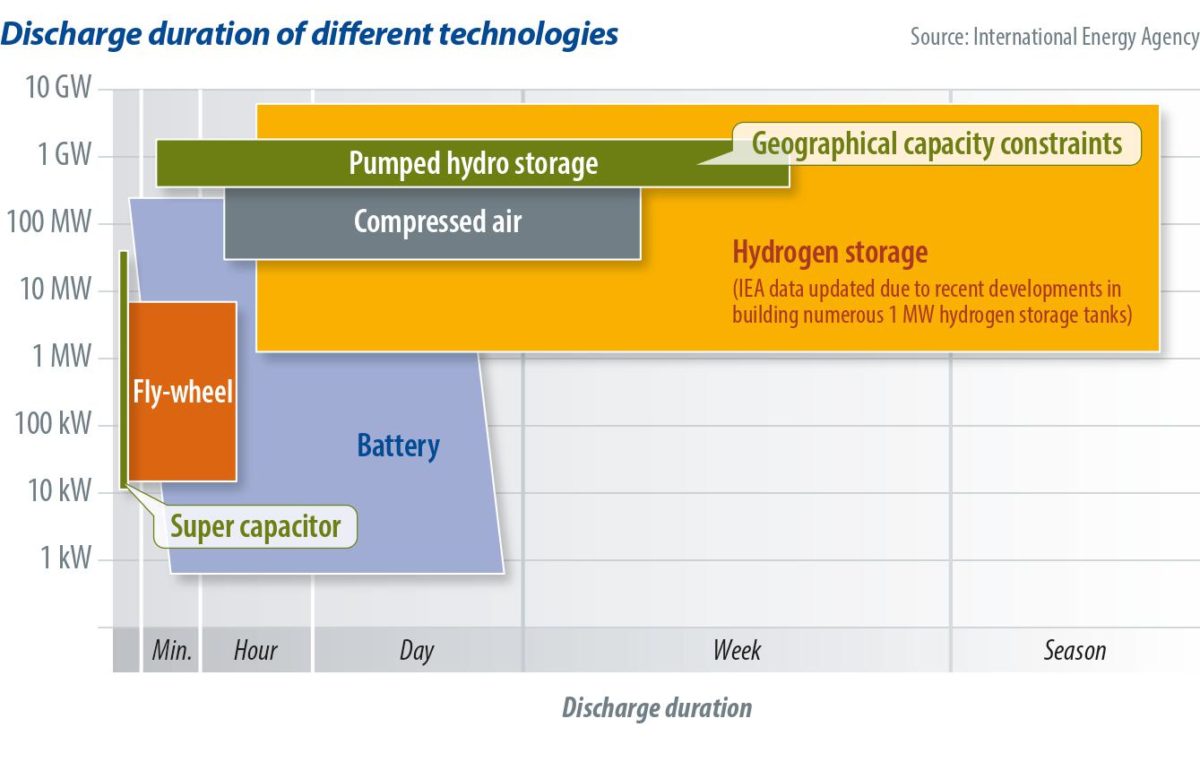

As you can see above, hydrogen for storage investments is included in the proposed ITC language. There can be no more important passage regarding hydrogen technology in the document than hydrogen storage qualifying for the ITC. 30% ITC until 2026 should give hydrogen a strong advantage to scale given large scale storage with hydrogen has better economics than any other technology even without an ITC. With a 30% ITC, large purchase orders for salt cavern geologic hydrogen storage, multiple tank pressurized hydrogen storage, and ammonia (NH3) storage will be written quickly. Hydrogen storage is up to an order of magnitude cheaper than lithium ion batteries in extended duration megawatt hour storage. Manufacturers of hydrogen production equipment should be able to use this ITC to highly leverage their scaling advantage as part of the storage process for green hydrogen. This would allow for rapid reduction of greenhouse gasses.

Clip from page 73:

Rep. Paul Tonko (D-NY) introduced the American Energy Opportunity Act of 2019 (H.R. 5335), which would establish a process to standardize permitting for distributed energy systems, including distributed renewable energy generation from solar, wind, hydrogen electrolysis and fuel cell systems, energy storage, electric vehicle (EV) chargers, and hydrogen fuel cell refueling.

This clip is highlighted because it was one of many similar passages: mentioning hydrogen in the same sentence as other distributed energy systems without hesitation and in the same regard as other solutions. It demonstrates a paradigm shift away from over ten years of FUD & stonewalling against hydrogen. Hydrogen has now performed a decade of demonstrations on the longevity & durability of fuel cell stacks in all temperatures & environments. The successful demonstrations in all forms of transportation & stationary performance for over ten years has silenced the hydrogen myths & critics. Hydrogen has been safely deployed in busses, trains, cars, airplanes, buildings and maritime vessels for years now. It’s legitimacy is accepted and 2020 starts the decade of hydrogen scaling.

Clip from page 90:

In May 2019, Reps. Mike Levin (D-CA) and Joe Neguse (D-CO) introduced H.R. 2764, the Zero-Emission Vehicles Act of 2019. Sen. Jeff Merkley (D-OR) introduced the Senate companion (S. 1487). The bill requires that 50% of sales for new passenger vehicles be ZEVs by 2030. The sales requirement ramps up 5% each year to achieve 100% of new vehicle sales by 2040. The bill is technology-neutral, allowing for electric vehicles, hydrogen fuel cell vehicles, and other potential zero-emission technologies to qualify.

Theme developing that I like about the document is just about everywhere there was talk about helping zero emission transportation develop, electricity & hydrogen were mentioned in tandem without debate and with equanimity. It’s working that people are starting to understand that electricity & hydrogen work together, not against each other. They’re truly cousins that share an anode & a cathode in their fundamental DNA. The only difference is one keeps its energy “inside the house” and the other keeps its energy “in the barn out back”. Batteries & hydrogen are darn near the same thing, so it’s good to see them starting to be recognized as cousins working together to replace fossil fuels with camaraderie.

Clip from page 126:

The public and private sectors are unlikely to adopt zero-emission trucks at scale until the supporting fueling infrastructure is convenient and widespread. CALSTART estimates that converting the nation’s trucking infrastructure to support zero- or near-zero-emission fuels will require $50 billion to $100 billion in public and private investment.329

The Clean Corridors Act of 2019, introduced by Sen. Tom Carper (D-DE) as S. 674 in the Senate and Rep. Mark DeSaulnier (D-CA) as H.R. 2616 in the House, provides grant funding to state, local, and tribal governmental entities to facilitate installation of electric charging stations and hydrogen fueling infrastructure along designated corridors in the National Highway System. The bill envisions that this infrastructure would have to accommodate large vehicles, including semi-trailer trucks.

The passage above was a gem of a find for RMP. Actually the bit that was so cool to find was footnote #329 which explains a $137 million dollar investment in electric charging & hydrogen refueling infrastructure throughout key cross country corridors for heavy duty trucking. Not only is this fantastic news on its face, the link also had GIS mapping of these hydrogen corridors which is the first time I’ve ever seen that. This will allow RMP to lift those latitudes & longitudes to add these future “hydrogen corridors” to our Google Map of all hydrogen refueling infrastructure in the USA. RMP’s map of hydrogen refueling infrastructure can be found here & is constantly being updated: https://www.respectmyplanet.org/hydrogen/north-america/infrastructure

Clip from page 257:

To achieve wide use of hydrogen at a reasonable cost, industry will need infrastructure to generate and transport hydrogen to facilities and to store hydrogen before and after transport. One option is to generate hydrogen at a small number of large-scale facilities and then distribute it through a pipeline network to individual industrial facilities. Another option is to generate it at a larger number of more dispersed, small-scale facilities, which would require less distribution infrastructure. Instead of transporting hydrogen directly, hydrogen producers could also transform the hydrogen into ammonia or methane for transport or storage.

This important passage mentions supporting technology to transform hydrogen into methane & ammonia. The word being used throughout the document is “building block” and there’s a heavy focus on industrial applications. One of the things I have always thought people failed to realize is the connection between industrial applications and transportation. When industry starts creating more & more hydrogen, it becomes more ubiquitous for refueling. When it becomes more ubiquitous for refueling, people will look around to each other and realize the chicken/egg problem they’ve been talking about for over a decade has miraculously solved itself. The next chicken/egg joke will be that people will ask: which came first the hydrogen vehicle or the hydrogen refueling station?

After about page 276, the document shifts to political wrangling of who is going to finance this massive overhaul of our energy sector. The document goes into other areas after page 276 like carbon removal, taxing people who produce carbon intensive energy, and carbon taxes in general. Basically, this is the part when you ask “Who’s going to pay for all this?” and the current companies that are dying are going to be asked to pay for the initiatives. This is the part where I really think we need to work together to train our workers in current industries to do new jobs in new industries. We cannot throw the baby out with the bath water so to speak. We must let fabricators, production managers, warehouse personnel, engineers, and the like find pathways to jobs in a zero emission future from their current jobs to produce fossil based energy. We cannot give all subsidies to startups with no track record while tax paying workers lose their jobs through this transition. We must make sure we create good jobs & a tax paying base with people from industries that will be phasing out.

Please read document yourself as I only picked a couple selected passages out for review. There’s a ton more information in there at 547 pages. Thanks for reading RMP’s little review of this big document as it relates to hydrogen production & storage infrastructure.

Leave a Reply